Weak Rupee, Higher Dirham Cost: Why Indian Investors Are Reassessing Dubai Property Timing

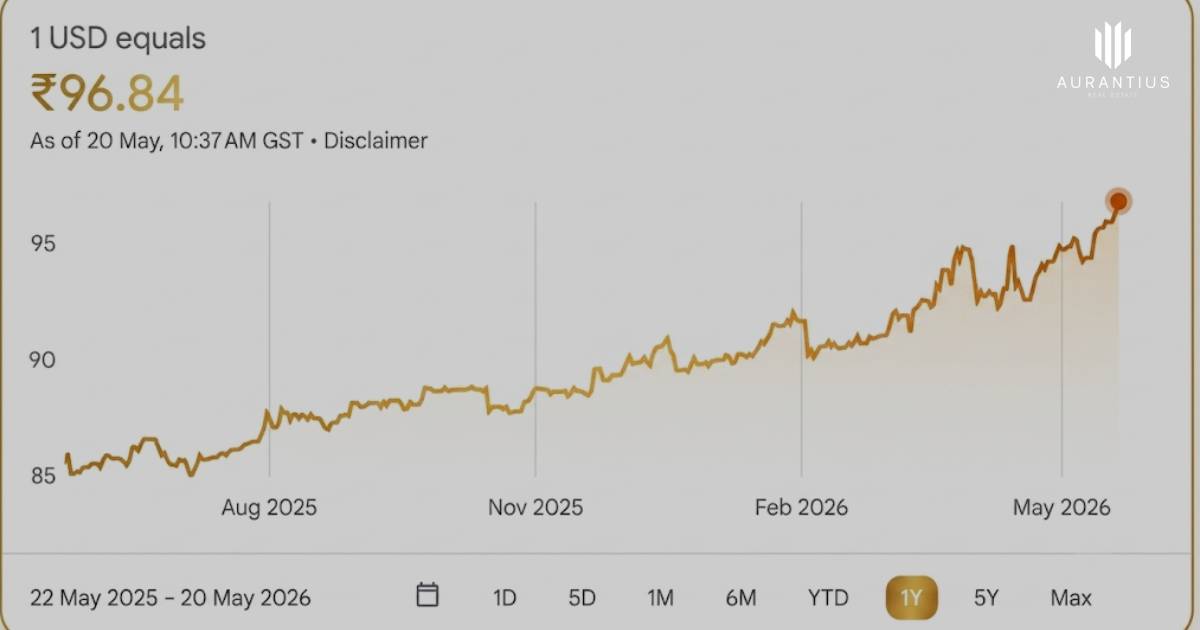

Don’t wait to buy UAE real estate. Indian investors evaluating overseas real estate, the cost of waiting to buy property in Dubai is no longer shaped only by apartment prices, rental demand, or launch timing. Currency movement now plays a direct role. The Indian Rupee weakened sharply against the US Dollar in 2026, with the exchange rate touching a record low near ₹96.96 per US Dollar on 20 May 2026. Since the UAE Dirham is closely pegged to the US Dollar, any sustained Rupee weakness can increase the effective INR cost of a dirham-priced property even when the Dubai selling price remains unchanged.

This creates a clear issue in the Indian Rupee to UAE Dirham real estate equation. A Dubai property priced at Dh1 million represents a very different rupee commitment depending on the exchange rate. At ₹85 per US Dollar, the implied rupee value of that Dh1 million asset is about ₹2.31 crore. At ₹96.96 per US Dollar, the same Dh1 million property is about ₹2.64 crore before Dubai transaction costs, legal expenses, or any rise in the property’s AED valuation. The property has not changed. The buyer’s purchasing power has.

That currency gap matters for Indian families planning to invest in Dubai real estate from India through savings, business profits, or long-term capital allocation. A delayed purchase may expose the investor to two separate risks: a weaker Rupee against the dollar-linked Dirham and a higher entry price if the selected Dubai asset appreciates during the same period. This is why the weak Rupee USD peg property asset discussion has moved from a macroeconomic topic into a practical purchase-planning issue for cross-border buyers.

Why Dubai Property Is Being Studied as a Currency-Linked Asset

Dubai real estate is increasingly evaluated by Indian buyers not only as a property investment, but as a hard asset denominated in a stronger regional currency framework. The UAE Dirham’s US Dollar peg gives investors visibility on the currency side of the transaction. For buyers holding a large portion of their net worth in Rupees, the appeal lies in shifting a portion of capital into an AED-priced asset that can generate rental income, retain long-term utility, and potentially appreciate alongside Dubai’s property market.

This analysis is especially relevant for investors comparing residential demand across established and emerging districts. Areas such as Dubai Marina, Downtown Dubai, Business Bay, Palm Jumeirah, Jumeirah Village Circle, and Dubai Hills Estate each serve different investor goals based on pricing, rental demand, tenant profile, and resale liquidity.

Investors also compare developer track records because capital protection in Dubai is not only about currency. Delivery reputation, project location, payment structure, and resale depth matter. Buyers frequently study brands such as Emaar, DAMAC, Sobha Realty, Nakheel, Meraas, and Select Group when reviewing both ready and off-plan opportunities.

Why Real Estate is Outperforming Gold for IndiansConsistent Passive Cash Flow

Gold acts as a dead asset because it sits in a vault and generates no monthly cash. Conversely, Dubai real estate offers net rental yields of 6% to 9%, completely tax-free. By comparison, rental yields in Indian metro hubs like Mumbai or Gurgaon struggle at just 2% to 3%.The US Dollar Currency Hedge: The UAE Dirham (AED) is pegged directly to the US Dollar. Because the Indian Rupee (INR) historically experiences depreciation against the dollar, holding UAE property provides a direct currency shield. Indian investors make double gains—from property appreciation and from the rising strength of the dollar-pegged Dirham against the Rupee.Residency Upgrades (Golden Visas): Buying gold cannot earn you a visa. However, investing in UAE real estate unlocks immediate residency privileges. Property purchases valued at Dh2 million or more qualify the buyer and their entire family for a 10-year renewable Golden Visa.

| Feature | Gold Investment | UAE Real Estate Investment |

|---|---|---|

| Primary Utility | Short-term inflation hedge & wealth preservation | Long-term capital growth & passive income generation |

| Recurring Income | None | High, predictable rental yields (6%–9% tax-free) |

| Tax Implications | High import duties and taxes when moving bullion across borders | Zero income tax, zero capital gains tax, and no rental tax |

| Residency Benefits | None | 2-year Investor Visa or 10-year Golden Visa options |

How Off-Plan Payment Plans Can Reduce Currency Timing Pressure

One practical response to exchange-rate uncertainty is the Dubai off plan payment plan currency hedge strategy. Instead of converting a large Rupee amount into Dirhams at one moment, a buyer may consider a regulated off-plan project with staged payments spread across construction milestones. This does not eliminate currency risk, yet it can distribute the conversion requirement over time and preserve liquidity during the purchase cycle.

Indian investors reviewing this route often assess projects based on payment schedule, location fundamentals, delivery timeline, and target tenant demand. Current search patterns commonly include developments such as Breez by Danube, Pearl House 4 by Imtiaz, Golf Verge, Rove Home Marasi Drive, Skyvue Spectra by Sobha, and Twilight by Binghatti. The objective is not to chase every launch, but to identify assets where payment structure and long-term demand remain aligned.

Regulatory discipline remains essential. Dubai’s off-plan framework requires buyer funds for sold units to be deposited into project escrow accounts linked to the development. This protects the transaction process and makes due diligence on project registration, escrow details, and developer compliance a core part of any purchase decision. Investors evaluating off-plan property should treat payment destination, project approval, and contractual clarity as non-negotiable checks.

What Indian Investors Need to Know Before Buying UAE Property

Can Indian residents legally remit funds to buy property abroad? Yes, within the applicable regulatory framework. Under the Reserve Bank of India’s Liberalised Remittance Scheme, resident individuals may remit up to USD 250,000 per financial year for permitted current or capital account transactions, including overseas property purchase. Family members can each use their own LRS entitlement where ownership and remittance conditions are structured correctly.

What cash-flow issue should buyers prepare for? TCS treatment under India’s remittance rules can materially affect immediate liquidity. For LRS remittances used for purposes other than education or medical treatment, tax collection at source applies at 20% on amounts above ₹10 lakh in a financial year. This is important for purchase planning because the tax collection mechanism can raise the upfront rupee cash requirement, even where the amount may later be available for tax credit or adjustment according to the investor’s filing position.

Can foreigners buy Dubai property? Foreign ownership is allowed in designated freehold areas, which is why cross-border buyers often study locations with clear ownership rights, established transaction depth, and broad tenant appeal. Investors who need a broader legal overview may review Can Foreigners Buy Property in Dubai? Complete 2026 Guide and Buying Property in Dubai as a Foreigner: Step-by-Step Process for 2026 before finalising the route.

Does UAE real estate support residency planning? Property investment can support long-term residency pathways where the buyer meets the relevant eligibility conditions. Official UAE guidance references AED 2 million real estate ownership within the investor-residency framework, subject to the governing authority’s requirements, documentation, and approval standards. Investors should treat residency as a structured eligibility matter, not as an automatic outcome attached to every purchase.

Why the Weak Rupee Changes the Timing Conversation

The central issue is not whether every investor should rush into a purchase. The more precise question is whether an Indian buyer who already intends to acquire UAE real estate should ignore the exchange-rate component of the decision. A weaker Rupee can raise the INR equivalent of the same AED-priced asset. That changes affordability ratios, down payment planning, LRS usage, TCS cash-flow needs, and the number of units or asset categories accessible within a fixed rupee budget.

This is also why Indian participation in Dubai property has gained attention in 2026. Buyers are studying the market through a broader capital-allocation lens that includes hard-currency exposure, international diversification, long-term rental demand, and cross-border family planning. For readers tracking this trend in more detail, Why Indian Investors Are Dominating Dubai Real Estate in 2026 provides additional context on the shift in buyer priorities.

From an investor perspective, the most practical approach is disciplined rather than emotional. The buyer should assess exchange-rate sensitivity, project quality, location demand, regulatory structure, remittance limits, TCS impact, and exit strategy together. A lower advertised property price does not automatically mean a better investment if currency pressure, weak rental appeal, or poor delivery profile reduce the overall quality of the allocation.

Conclusion: Currency Risk Is Now Part of the Dubai Property Decision

The Indian Rupee’s weakness against the US Dollar and UAE Dirham has made cross-border property timing more consequential for Indian investors. A Dubai asset priced in Dirhams can become significantly more expensive in rupee terms without any change in the property’s listed AED price. That effect becomes more important for buyers who already plan to enter the market, use LRS remittances, explore off-plan payment structures, or build long-term exposure to Dubai’s residential sector.

The investment case should remain grounded in fundamentals. Currency protection alone is not a sufficient reason to buy a property. Strong location selection, credible developers, regulated payment processes, realistic rental expectations, and a clear holding period still determine whether a Dubai purchase supports the investor’s financial objectives. The Rupee trend simply adds urgency to the need for accurate planning and disciplined execution.

Aurantius Real Estate helps investors evaluate Dubai property opportunities through a structured, market-focused approach that considers location strength, developer credibility, payment schedules, off-plan risk, and long-term investment suitability. Indian buyers assessing UAE real estate in a weaker-Rupee environment can use informed guidance to compare options clearly and move with stronger financial discipline.